In the wake of Russia’s invasion of Ukraine in February 2022, Europe’s energy markets have experienced high electricity prices and multiple gas supply disruptions that have prompted a dramatic rethinking of European energy security strategy. While Europe has been able to withstand the brunt of the energy crisis so far thanks to a relatively mild winter and ample reserves of Russian gas, it is gearing up for a more difficult winter season next year.

Depending on how the war develops in 2023 and how committed European countries prove to be to their sanctions against Russian oil and gas imports, this year may provide several opportunities to develop Israel’s gas export potential, oil transit and storage capabilities, and renewable energy sales. While these opportunities could be rewarding, they entail economic, security, and environmental risks that need to be taken into consideration.

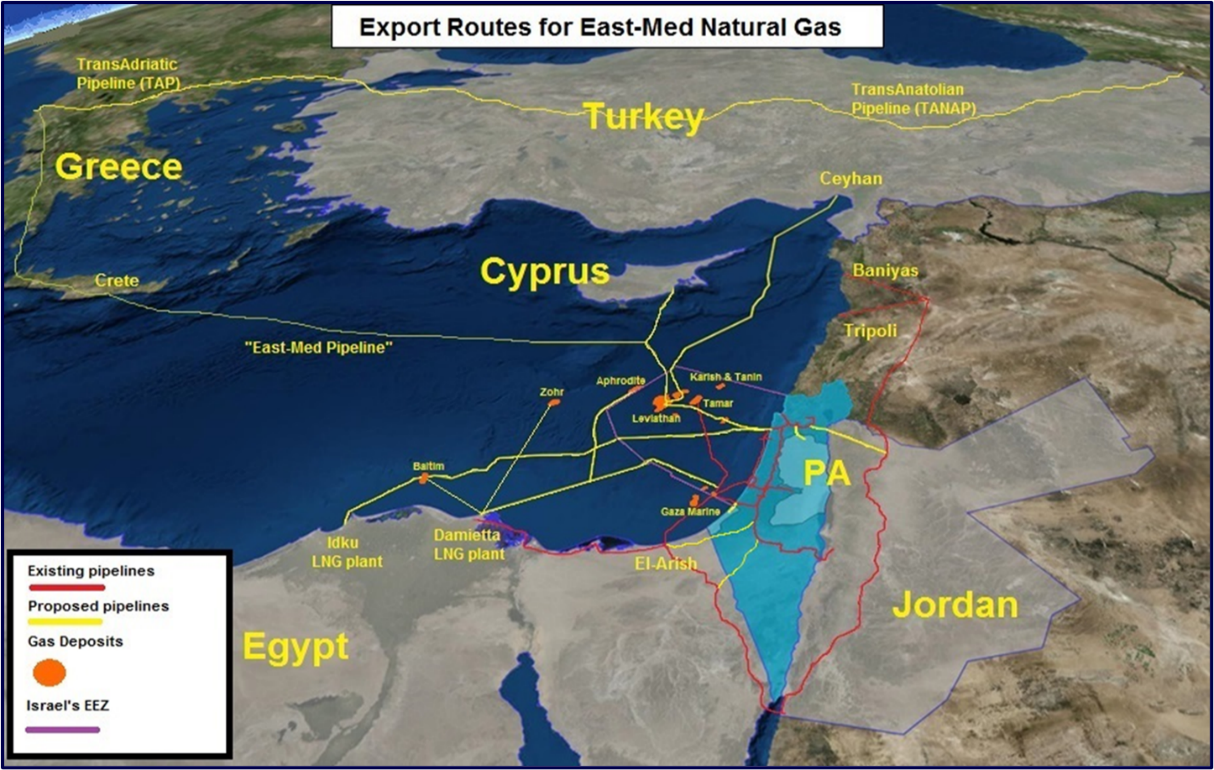

- Increased Potential for Israeli Gas Exports

Ever since the discovery of major offshore gas deposits in 2009 and 2010, Israel has been struggling to secure major export deals to Europe. Several hurdles, including the relatively small amount of gas available for export, the challenging topography of the Eastern Mediterranean Sea, and political feuds over maritime borders have made it too expensive and risky for private companies to invest the billions of dollars needed to construct an underwater pipeline from Israel to Europe. As a result, Israel has yet to find buyers for about two-thirds of the gas it has earmarked for export and has seen its bidding rounds for new gas exploration licenses repeatedly fail.

This could change following the Russian invasion of Ukraine, which caused a major price hike for imported gas in Europe and a new desire among EU policymakers to secure non-Russian gas supplies even at higher cost, especially liquified natural gas (LNG).

These developments in Europe are important for Israeli gas prospects because up to now, Israel’s two main potential export destinations have proven out of reach on both economic and political grounds: a pipeline to Greece and a pipeline to Turkey. The idea of an underwater pipeline from Israel to Greece through Cyprus (the East-Med Pipeline) excited policymakers in all three countries and spurred a series of high-profile meetings and agreements, but has yet to yield tangible results. The economic viability of such a pipeline has proven too difficult due to geographic and technical limitations.

If constructed, the East-Med pipeline would be the longest and deepest underwater pipeline in the world, reaching depths of 2,000 meters (compared to Nord Stream 2, which reaches a maximum depth of 210 meters). This depth limits how wide the diameter of the pipeline can be without collapsing in on itself, thus decreasing the amount of gas that can run through it. The East-Med would also need to run through areas near Crete that experience seismic activity, meaning its construction would entail multiple engineering challenges that will make it much more expensive.

These challenges can all be overcome, but will require that the end user (Greece) agree to pay a high fixed price for the gas as part of a 10–15-year binding contract to justify the costs of the pipeline. Initial estimates are that Greece will need to pay around $8 per MMBtu, while the average price of gas in Europe in recent years has hovered between $2-6 per MMBtu. Neither the Greek government nor any private companies have been willing so far to commit to such a deal. Adding to these complications is the feud among Greece, Cyprus, and Turkey over who controls the maritime territory through which the pipeline will need to pass.

Figure 1: Existing and Potential Gas Pipelines in the East Mediterranean

Source: Delek Group Ltd, Presentation for Investors, October 2017. Additional graphics: Elai Rettig

The economic and political impasse surrounding the East-Med pipeline to Greece has reawakened the dormant Israel-Turkey option. Turkey is a large natural gas market with an existing infrastructure (the TANAP pipeline) that can transit gas to Europe, making it — at least in theory — a good candidate for Israeli gas exports. However, attempts in 2015 to promote an underwater pipeline between Israel and Turkey failed over price disagreements and political tensions. Turkey demanded a lower price for the gas than the private gas companies could offer due to Israeli regulations. Israeli officials are also wary of Israel’s becoming too dependent on Turkey as its primary gas customer due to fears that Turkey will use the pipeline as a political tool.

Before signing such a deal, Israel would need to protect itself from deliberate disruption by securing assurances supported by third-party guarantees from either the US or the EU. For its part, the European Union has not been keen on the idea of bolstering Turkey’s position as Europe’s main gas transit country (in addition to its role in transiting gas from the Caspian region, Russia, Iraq, and potentially Iran), as doing so would grant Ankara economic and geopolitical advantages in its dealings with Europe.

The dramatic rise in European gas prices following Russia’s invasion of Ukraine has changed some of the EU’s calculations, but not enough to justify a major pipeline deal to either Greece or Turkey. As prices have reached $25 per mmBTU in some European gas hubs, it may seem that expensive gas pipelines from the Eastern Mediterranean make much more sense than they did two years ago. However, it is not clear how long these high prices will hold. In some places, they have already dropped to pre-war levels.

A major infrastructure project from the Eastern Mediterranean to Europe can be completed by the end of 2025 at the earliest. But will the war in Ukraine still be going on in 2025? Will there still be sanctions against Russian gas? Will Putin still rule Russia? Until European investors know the answers to these questions, it is still a very risky prospect for the private sector to invest in multi-billion-dollar infrastructure. Unless the European Union provides guarantees that private investors won’t lose their investments once prices go down, Israeli gas companies are unlikely to be able to lock down a 10–15-year binding contract with a European customer.

The culmination of these political, economic, and technical limitations has pushed European customers to bet on the LNG option. For Europe, LNG imports offer more flexibility to search for non-Russian suppliers, freedom from transit states, and a quicker solution to the gas crisis than pipelines. While most efforts to build LNG intake terminals (i.e., regasification facilities) in Europe over the past decade have focused on Western Europe, the current crisis is pushing towards more terminals in central and southeastern Europe (including Greece, Italy, Poland, Germany, and Estonia).

Assuming the EU goes through with building these new LNG terminals and increases LNG demand over the next two to four years, it will still need to compete with Asia for demand. Europe has been lucky so far in that it did not need to compete with East Asia for LNG during 2022 due to a mild winter and COVID restrictions in China. But 2023 may see a surge in East Asian demand for LNG as China recovers from lockdowns, and the price may increase substantially. This will require much more LNG supply to come online in the next few years.

Israeli and regional investors are hopeful that LNG will be the next chapter for the East-Med gas export market, ridding it of the geopolitics of pipelines. The cheapest and most immediate option for Israel to export LNG to Europe would be to do it through Egypt’s two existing LNG terminals at Idku and Damietta. However, this does not represent an ideal solution. There is not much spare capacity left at those terminals to increase exports, they do not have the most efficient technology (a considerable amount of gas is lost during liquification), and they offer more geopolitical advantages to Egypt than to Israel. In addition, Israel needs to overcome infrastructure bottlenecks that are preventing it from exporting more gas to the LNG plants in Egypt. A new direct underwater pipeline will need to be built from its gas fields directly to the terminals.

Other LNG export options may exclude Egypt but contain challenges of their own. Israel can lease or purchase a floating LNG (FLNG) facility, which is cheaper and creates much less political pushback (i.e., NIMBY opposition over the shoreline in Israel). However, most FLNG ships generate only small amounts of gas (0.5-2 BCM annually), and even the biggest FLNG offers much less capacity to export compared to a regular land-based LNG terminal (4-6 BCM annually vs. 12 BCM).

Another option would be to construct a land-based LNG terminal in Cyprus. However, this might anger Egypt, which aspires to become the “LNG hub” of the Eastern Mediterranean. It could also create problems with Turkey over contested political waters around Cyprus.

- Turning Israel into an Oil Transit Route to Europe

In addition to raising natural gas prices, the war in Ukraine is causing a major shift in global oil transit routes, putting the Eastern Mediterranean, and particularly Israel, right in the middle. As European sanctions against Russian oil come into play at the beginning of 2023, Russian oil is heading towards East Asia instead (e.g., China and India). Some of this oil is shipping through the Northern arctic route (which is more available to Russia due to climate change and melting glaciers), and some is going through the Eastern Mediterranean and the Suez Canal.

Russian oil is being sold at a deep discount and is accordingly grabbing market share at the expense of the Gulf States, including Saudi Arabia, the UAE, Qatar, and Kuwait. In return, Europe is asking for more oil from the Gulf to compensate for the loss of Russian oil, which means more Gulf oil is flowing West through the Suez Canal and the Eastern Mediterranean to reach European markets.

This reconfiguration of global oil routes can reignite and even expand Israel’s role as a transit and storage destination for Europe-bound oil via the EAPC pipeline. Over the past two decades, the Europe-Asia Pipeline Company, previously the Eilat-Ashkelon Pipeline Company (EAPC, or KATZAA in Hebrew), has been a minor player in storing and moving Russian, Azerbaijani, and Kazakh oil from north to south (Ashkelon is in the Eastern Mediterranean and Eilat is on the Red Sea), thus reducing the costs of transit through the Suez Canal. Following the Abraham Accords, Israel signed a deal to transit UAE oil from south to north (Eilat to Ashkelon), reversing the flow of the pipeline and substantially increasing the amount of oil it transfers. The deal quickly created controversy in Israel due to the substantial environmental risks that increased oil movement in the Eilat bay could cause to marine life and the tourism industry in case of accident, and the deal became mostly dormant. However, a combination of pressure from the US and Europe to help move cheaper Gulf oil through the Red Sea during this time of crisis, along with the new Netanyahu government’s keen desire to expand relations with the UAE (and perhaps the Saudi kingdom), may revive the UAE-EAPC deal.

Figure 2: Existing and Potential Oil Transit Routes via the EAPC

![]()

Source: Europe Asia Pipeline Company Website, Digital Magazine. Additional graphics: Elai Rettig

More oil flowing to Europe through Israel and Egypt entails considerable environmental and security risks for both the Red Sea and the Eastern Mediterranean Sea. Potential for oil leaks and accidents will inevitably rise along with increased movement of oil tankers, requiring more cooperation among the countries of the region in standardizing monitoring and quick-response measures. The movement of Israel-bound oil tankers in the Red Sea may also increase potential for Iranian sabotage, especially near the Bab-el-Mandeb Straits, where they could be vulnerable to Iran-backed Houthi rebels in Yemen. Operations of this kind may be more appealing to Iran than operations in the Persian/Arabian Gulf and the Straits of Hormuz, which could block Iran’s oil shipments as well. Increased Iranian maritime threats require deeper cooperation among the region’s naval forces, a process that is already underway.

- A Brighter Future for Israeli Renewable Energy Technology

Finally, Europe’s energy challenges are creating a major push towards alternative energy solutions in both Europe and the Arab Gulf States, offering Israel a major role as a leader in clean-tech innovation. On the European side, while the energy crisis is causing a rise in demand for oil, gas, and coal in the short term, it is also encouraging further investment in solar, wind, and even nuclear alternatives to increase independence from Russian imports over the longer term. This should cause a substantial rise in clean energy project funding throughout Europe in the next few years, allowing Israel to bid for projects and take an active part in the transformation. This is especially relevant for Israeli innovation in solar energy, cyber defense for smart grids, and energy efficiency solutions. Other promising avenues may include hydrogen and energy storage technology innovation.

An additional market for Israeli innovation is the Arab Gulf States as they look for solutions to decrease domestic demand for oil and gas through alternative energy systems. Saudi Arabia, for example, loses almost a third of its oil production due to local demand in the form of heavily subsidized electricity generation and gasoline, as well as other subsidized products. As the Gulf States are experiencing a boom in population and a rise in the standard of living, this rising trend not only places a heavy burden on government budgets but also obstructs the Gulf’s ability to meet growing European demand as Russian oil sanctions revamp the global oil map. Israeli efficiency and solar innovation may thus help the Gulf States meet growing domestic demand while making more oil and gas available to European customers searching for non-Russian supply — a win-win for all parties.

(Written by Dr. Elai Rettig, lecturer and assistant professor in the Department of Political Studies and a senior research fellow at the Begin-Sadat Center for Strategic Studies at Bar-Ilan University. He specializes in energy geopolitics, national security, and international environmental policy)

{Reposted from BESA site}

{kind=link}